East Africa's Tech Funding Rebound: The Return of Regional Startup Investment

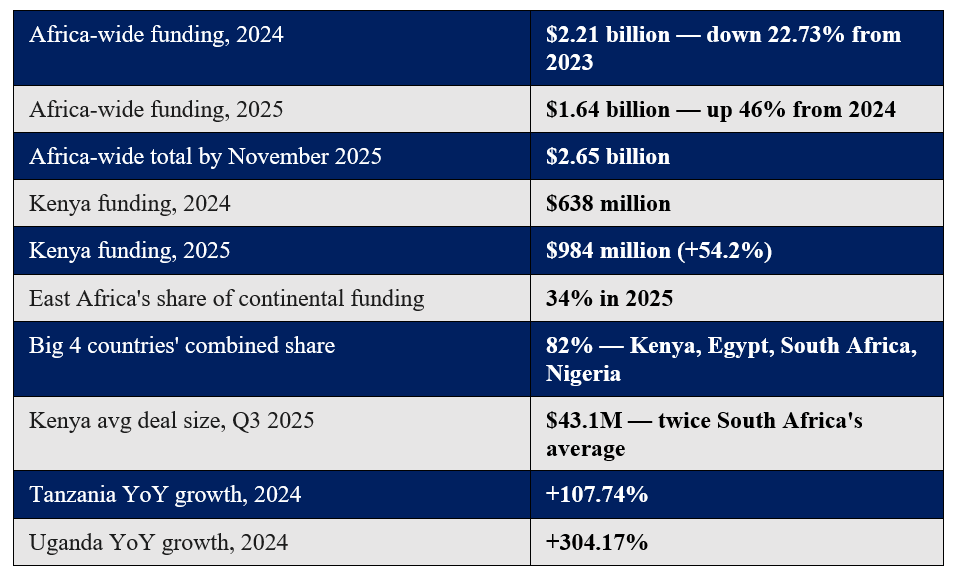

In 2025 alone, Kenya raised $984 million in startup funding, a figure that was nearly one-third of all startup money raised across Africa in the same year, and the best result the country had seen since 2022. This comeback was especially striking, given how bad things had become between 2022 and 2024 when global investors pulled back from emerging markets, leading to a nearly 23% drop in funding for African startups. However, 2025 saw a 46% rebound in startup funding to $1.64 billion across the continent, with East Africa leading the recovery.

Beyond funding recovery, the bigger story lies in the type of company getting funded, that is, the fundamental change from consumer apps to real infrastructure, from equity-only deals to structured debt, and from fintech dominance to clean energy and mobility. This article breaks down the changes, their regional contributing factors, as well as the opportunities and barriers.

The Funding Crisis

Between 2022 and the first half of 2024, rising interest rates in the US and Europe resulted in increased global caution from investors, and Africa, which was seen as a higher risk, was hit harder than most. Total VC funding across the continent fell to $2.21 billion across 488 deals in 2024, a drop of 22.73% from 2023. The continent’s number of active investors also fell from 987 in 2022 to just 330 by 2025. The first signs of recovery came in the second half of 2024, where funding went up by 24.96%, as compared to the same period in 2023, driven by two big fintech rounds: Moniepoint ($250 million) and TymeBank ($110 million). Both were established companies with real revenue, which signalled that investors were willing to back proven businesses again.

Kenya led the rebound in 2024, capturing $638 million, which was 88% of East Africa's $725 million total before jumping to $984 million in 2025, a 54.2% year-on-year increase. Kenya's average deal size in the third quarter of 2025 reached $43.1 million, twice South Africa's average, a sign that investors are placing large, confident bets on the region. Tanzania and Uganda also showed strong growth, Tanzania up 107.74% and Uganda up 304.17% year-on-year in 2024 showing that the recovery is spreading beyond Nairobi. Across the continent, 178 startups raised $1.64 billion in 2025, and by November that year, the cumulative total exceeded the full-year 2024 figure at $2.65 billion.

Key Contributing Factors Behind East Africa’s Rebound Success

Shift in Sectoral Interests

While consumer apps ride-hailing, food delivery, and e-commerce attracted most attention in 2021, current deals are in energy, transport, and agricultural tools, with funding switching to essential businesses that generate steady, predictable income. The reason is straightforward: there is a consistent demand for solar systems, electric transport, and irrigation tools to solve everyday problems.

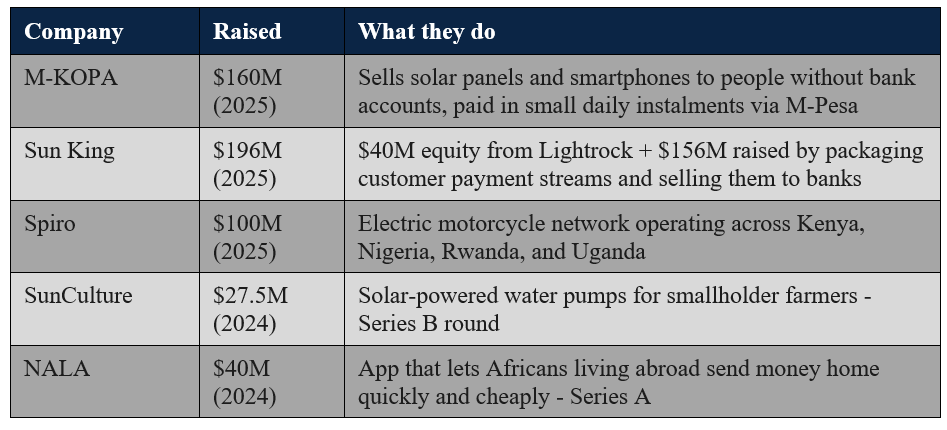

These companies also have physical assets, such as solar panels, motorcycles, and irrigation pumps, that can serve as collateral for loans. In fact, half of Africa's biggest startup rounds in 2025 were bank loans, not equity investments. Sun King combined $40 million in equity from Lightrock with $156 million raised by securitising its customers' future payment streams, a sophisticated structure that reduced its overall cost of raising money.

This puts clean energy technology businesses at an advantage, as illustrated by climate and clean energy funding, which fell to $754 million in 2024 but rebounded to $1.1 billion by November 2025. In the first half of 2025 alone, climate and energy startups raised over $219 million, making it the second-most funded sector on the continent after fintech.

Figure 2. Clean Energy Funding in Africa. Sources

While fintech remained the largest equity sector at $769 million, 25% of total equity raised across Africa, the type of fintech getting funded also shifted. Consumer banking apps are out of favor. What investors are backing are payment infrastructure and B2B tools. Cross-border payments are the standout opportunity: NALA raised $40 million, and Wave raised $137 million as a debt facility, both targeting the high cost of sending money across African borders.

Role of Government-backed investment funds (DFIs)

Currently, Government-backed DFIs are playing an essential role by getting private funding to flow back into developing markets. By absorbing some of the risk themselves, they give commercial banks and investors the confidence to join. Globally, the IFC (World Bank), the UK's BII, France's Proparco, and the US DFC are involved in almost every major regional deal. G7 governments collectively committed $80 billion to African businesses over five years through these bodies. When a DFI commits, it signals to commercial investors that the deal has passed serious scrutiny and that unlocks more capital.

Surge in European investors, African funds, and big corporates

European VCs and impact investors drove a surge in funding in September 2025, pushing the year's total past 2024's full-year figure with months still to go. African funds TLcom Capital, Partech Africa, Novastar Ventures, and Equator stayed invested through the quiet years and now hold an advantage that latecomers cannot replicate. Global names like Acrew Capital, DST Global, and Norrsken22 are returning selectively, and the arrival of Mastercard, Visa, Coinbase, Safaricom, and MTN as strategic investors signals that East Africa's digital economy is now large enough to be commercially valuable to some of the world's biggest companies.

Favourable Policies

The East African Community (EAC) allows startups to expand across Kenya, Tanzania, Uganda, and Rwanda using shared regulations. NALA, founded in Tanzania, now serves payment corridors across four countries and attracted investors like Acrew Capital and DST Global, who see the whole region as a single addressable market. Spiro deployed its electric motorcycles across four countries simultaneously.

Existing Barriers and Government Intervention

While early-stage funding has become more accessible in Nairobi, the $5–20 million growth stage remains severely underserved venture funds prefer later-stage deals, while DFIs target larger ones, leaving many proven startups unable to scale. Startups with at least $1,000 in Monthly Recurring Revenue money coming in reliably every month are 40% more likely to raise seed funding than those without it. Investors also prefer companies invoicing in US dollars or euros, since African currencies can lose value quickly and eat into returns.

Regional funding gaps present another challenge. Kenya dominates East African funding, with nearly all of it flowing to Nairobi. The notable growth in Tanzania and Uganda in 2024 is limited to a small base, meaning a startup in Dar es Salaam or Kampala still faces a structurally harder path to capital. Regulatory and currency headwinds add friction. Stricter compliance rules, such as Tanzania's 2% digital services tax, complex cross-border licensing, and Kenyan shilling volatility all weigh on investor returns and confidence. Exit routes also remain thin. East Africa has almost no track record of tech Initial Public Offerings (IPOs) and a limited pool of acquirers, meaning cautious investors are likely to stay on the sidelines until circumstances change.

However, regional governments are actively reshaping conditions for tech investment. Kenya has launched a National AI Strategy targeting health, agriculture, and finance, invested in the National Optic Fiber Backbone (NOFBI) for nationwide connectivity, and introduced a digital nomad visa to attract global talent and spending. Its energy grid, roughly 90% renewable, gives electric vehicle and solar startups a genuine clean credential that few markets can match. On the ground, M-Pesa's mobile money infrastructure and accelerators like iHub and Nailab provide the ecosystem support that investors look for before committing capital. Rwanda is streamlining business registration and digital regulations, positioning itself as a credible second hub in the region. Uganda, meanwhile, is updating its National Payment Systems Act to reflect how far digital finance has evolved since the early M-Pesa era.

Conclusion

East Africa's funding rebound is not just a bounce-back after a few bad years. The companies getting funded, the tools being used to fund them, and the investors committing capital have all fundamentally changed. The region is moving from speculative bets to substantive infrastructure, and that shift is what makes this moment different. If the middle funding gap closes, exit routes open up, and more capital reaches cities beyond Nairobi, East Africa has a credible path to becoming the continent's top destination for meaningful tech investment.