East Africa’s Export Surge: Momentum or Transformation

While global trade struggles through headwinds of protectionism and geopolitical tensions, East Africa is chartering a different course. In Q2 of 2025, exports from the East African Community (EAC) rose by 40.5% year-on-year to $18.6 billion. Yet, behind the headline figures sit two competing narratives. On one hand, a favourable commodity price cycle, notably record prices in both gold and coffee, has boosted export earnings across the region. On the other hand, both intra-regional and wider inter-African trade have expanded steadily as supply chains have shortened and economic integration deepened.

This contrast raises a critical question. Is the region’s export-led growth sustainable, or is it merely a windfall provided by a favourable market cycle? The answer will determine whether the prevailing momentum can translate into sustained, value-driven growth or fade as commodity cycles inevitably turn.

The Numbers Behind the Surge

The EAC’s trade performance in 2025 represents a decisive break from recent trends. The bloc’s exports followed 40.5%year-on-year growth in Q2 2025, with 32.3% year-on-year growth in Q3 2025 as they hit $19.6 billion. The growth reflects growing demand for East African goods as the region becomes more competitive in global markets.

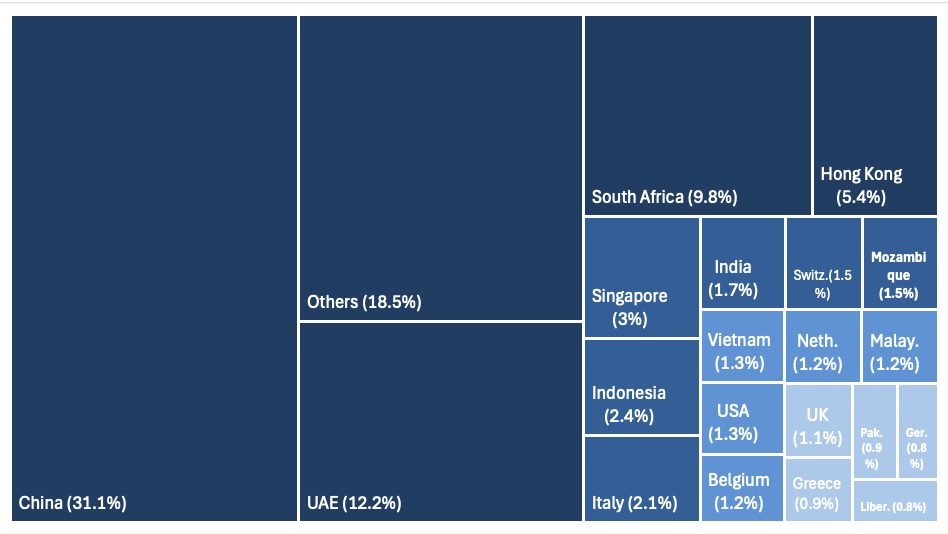

Trade within the East African Community expanded by 15% from $4.2 billion in Q3 2024 to $4.8 billion in Q3 2025. Similarly, intra-African trade continued to play a major role, rising to $10.1 billion, and accounting for 25.2% of the bloc’s trade. In particular, exports to South Africa were up more than 137% in the third quarter of 2025. The EAC’s top 20 export destinations over that same period are illustrated by the figure below.

Figure 1: EAC’s Top 20 Largest Export Markets (Q3 2025). Source

The Commodity Windfall

East Africa’s export boom has arrived on the back of a favourable global price environment for the region’s top exports . Gold surged close to 65% in 2025, as geopolitical tensions and the Trump administration’s disruption of global markets propelled the safe-haven metal to its best year since 1979. This proved particularly beneficial to Uganda, where gold exports increased 75.8% to $5.8 billion, and Tanzania, where they increased by 36%.

Concurrently, coffee prices have surged following weather-related supply disruptions. More specifically, droughts in the world’s two top producers, Brazil and Vietnam. This tightened global supply while demand continued to grow, pushing coffee prices to near a 50-year high reached in February 2025. This has created a perfect storm for the major coffee producers in the region including Rwanda, Kenya, Tanzania, Burundi and Uganda. Notably, Uganda emerged as the largest coffee exporter in Africa, over taking Ethiopia and earning a record $2.4 billion in 2025.

Similarly, copper prices have also remained elevated. According to the United Nations Conference on Trade Development (UNCTAD), this is primarily due to the sustained shift towards renewable energy, growing demand for electric vehicles and data centre construction. On the other hand, disruptions such as landslides, flooding and seismic activity plagued copper mining around the world and limited the growth in supply to just 1.3%. As a result, copper prices increased by 43.9% in 2025, contributing to earnings of $19.8 billion in the Democratic Republic of Congo and $2.2 billion in Tanzania.

Rise of Intra-Regional and Intra-African Trade

Beneath the commodity headlines lies a subtle yet potentially more transformative story. Africa is increasingly trading with itself. Intra-EAC exports surpassed $4 billion in Q2 2025, growing faster than exports to traditional partners in Europe and Asia. These numbers represent genuine progress in converting integration rhetoric into an economic reality.

The composition of intra-regional trade matters as much as the volume. Unlike exports to external markets, dominated by raw coffee, unprocessed minerals, and cut flowers, intra-EAC trade skews toward manufactured and processed goods. According to the United Nations Economic Commission for Africa (UNECA), agricultural produce and manufacture goods such as textiles, chemicals, pharmaceuticals and cement are driving the growth in East African trade.

Kenya’s Economic Survey 2025 offers a telling proxy for broader regional patterns. Manufactured exports to EAC partners grew 28% even as manufacturing exports to the rest of the world contracted. The divergence suggests that regional integration is creating market opportunities that globalization alone hasn’t delivered, particularly for firms producing consumer goods, building materials, and agro-processed products such as sugar, processed milk, maize, steel and cement.

However, commodities still play a pivotal role in regional trade. For instance, Uganda has become a hub for processing and re-exporting gold from neighbouring countries such as South Sudan, the Democratic Republic of Congo and Tanzania. Consequently, gold has overtaken coffee to become the country’s largest export as record prices attracted new entrants to the sector.

Similarly, Intra-African trade exhibits similar dynamics in terms of its nature and trajectory. Exports to South Africa, a world-renown hub for mining and mineral processing, almost tripled year-on-year in Q3 2025 as the country emerged as an increasingly important destination for Tanzanian gold and Congolese copper and cobalt. Tanzanian gold exports to South Africa have more than doubled since 2020.

Infrastructure improvements are accelerating these trends. One-stop border posts, despite persistent inefficiencies, have reduced clearance delays. Digital trade documentation is slowly replacing paper-based systems that historically added days to regional shipments.

Perhaps most importantly, intra-regional trade has proven more resilient to external shocks. According to UNECA, when COVID-19 disrupted global supply chains, regional trade routes adapted faster. When the Ukraine war sent shipping costs soaring, intra-EAC trade continued largely unaffected[MA1] .

Structural Limits

Despite recent export gains, East African trade continues to grapple with some persistent challenges. Intra-regional trade still represents only 12.1% of the EAC’s total exports and manufactured foods accounted for just 17.5% of regional exports. On the other hand, raw commodities, such as gold and copper, dominate and make up 53% of intra-EAC trade. Modest compared to the EU where 64% of trade takes place within the bloc and 78% of goods exported within the region are manufactured products.

Furthermore, there remains considerable barriers to trade within the EAC. Despite the establishment of the East African Customs Union as well as the Common Market Protocol, Tazania’s 2025 Finance Act introduced excise duty on imports from fellow EAC Member States. These included an Industrial Development Levy and additional excise duties between 10% and 15% on imported goods. While such shifts in national fiscal policy have been successfully challenged at the East African Court of Justice, it highlights the fragile nature of regional trade.

Infrastructure and logistics gaps compound these structural weaknesses. Traders across the region still contend with punishing transport costs and chronic delays. Landlocked producers face especially steep premiums, paying more for deteriorating roads, congested ports, and bureaucratic customs procedures. Underdeveloped transport corridors and elevated freight costs continue to blunt the potential of regional value chains.

Trade finance constraints tighten the squeeze further. Afreximbank’s 2025 Trade Report estimates an annual African trade finance gap of approximately $100 billion, limiting access to credit for SME exporters and intra-regional commerce. Furthermore, trade finance for intra-African transactions remains more expensive and harder to access than finance for exports to Europe or Asia, a paradox that constrains even willing regional buyers.

Locking in Gains

Turning export momentum into durable transformation requires moving fast while commodity prices remain favourable and thinking beyond them. Firstly, regional industrial policy coordination must shift from aspiration to execution. The EAC needs targeted support for sectors where intra-regional value chains are already emerging, pharmaceuticals, agro-processing, textiles, and construction materials. Coordinated investment in these industries can deepen manufacturing linkages before the next commodity downturn.

Secondly, infrastructure investments must focus on trade-critical bottlenecks: port efficiency, digital customs integration, and transport corridor reliability. Recent gains from the Single Customs Territory prove that targeted reforms deliver measurable results. Finally, deeper African Continental Free Trade Area (AfCFTA) engagement offers the EAC a pathway beyond its own market constraints. Preferential access to West and Southern African markets can absorb the region’s growing manufacturing output and reduce vulnerability to any single trading partner.

Conclusion

Whereas East Africa’s export surge is impressive, its durability remains contested. Record prices for gold, coffee, and copper have clearly amplified export earnings, offering a timely boost to foreign exchange inflows and fiscal space. Yet, the evidence suggests that prices alone do not explain the breadth of recent gains. The steady rise of intra-regional and intra-African trade, particularly the expansion of manufactured and processed goods within the EAC, points to deeper structural shifts underway. These trends matter because they are less volatile, more value-intensive, and more closely tied to domestic production and employment.

Still, momentum should not be mistaken for transformation. Manufacturing’s limited share, persistent infrastructure gaps, policy reversals, and a severe trade finance shortfall threaten to cap progress once commodity cycles turn. The challenge for the EAC is therefore not whether it can export more, it already is, but whether it can convert today’s favourable conditions into a more resilient, diversified, and regionally anchored growth model. The window to do so is open, but it will not remain so indefinitely.